An AI-generated scene… but the bill is all too real.

EOFY Celebrations Are On — Who’s Picking Up the Tab?

Managing Director & Co-founder

Hamilton12 | Evidenced-Based, Systematic Investment Strategies

July 13, 2025

As annual reports arrive, investors may find they’ve covered more of the bill than they thought.

It’s that time of year when fund managers report financial year performance and EOFY celebrations take centre stage. But while managers and their investors toast another year of returns, something more sobering is landing quietly in inboxes and on websites: managed fund annual reports.

And inside those reports is a less festive question — who’s actually picking up the tab?

When we set out to establish Hamilton12 and our flagship Australian Shares Income Fund, the intention was simple: offer investors a transparent, tax-aware strategy built around a proprietary S&P Dow Jones Indices index. From day one, we made a conscious decision to charge only a low management fee and an aligned performance fee — the costs directly tied to delivering investment outcomes.

What surprised us was learning that it’s standard practice for many funds to charge additional expenses — including trustee oversight, custody, registry, and administration — to the fund itself. For us, these were operational costs we had always assumed would be met at the manager level. We never considered passing them on. The reason was straightforward: these costs reduce investor returns over time, and our goal has always been to maximise what investors keep.

This experience opened our eyes to a broader question: do investors — and their advisers — fully understand what they’re paying for?

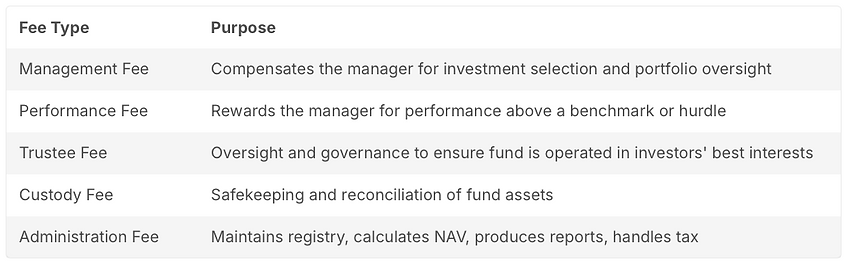

Most are familiar with the management fee. This is what investors pay for the expertise of the fund manager — selecting investments, managing risk, and running the portfolio. But that’s only part of the story.

Managed funds often have a trustee, also known as the Responsible Entity, whose job is to provide governance and ensure the fund is being operated in the best interests of investors. That oversight carries a fee — typically 0.05% to 0.10% per annum — which in many cases is paid out of the fund itself. It’s a curious arrangement when the cost of keeping a fund manager accountable is charged not to the manager, but to the very investors the oversight is meant to protect.

It’s a curious arrangement when the cost of keeping a fund manager accountable is charged not to the manager, but to the very investors the oversight is meant to protect.

Then there’s custody: the safekeeping of the fund’s assets. The custodian ensures shares and other securities are held securely and reconciled properly. That too incurs a cost. Yet here again, it’s the investor footing the bill to make sure their money is actually where the manager says it is.

Administration fees cover essential back-office tasks — maintaining the unit registry, calculating the fund’s daily price, preparing financial reports, and coordinating tax statements. These services are critical to operating the fund but also attract additional expense. They’re fundamental to running a fund, yet it’s the investor who pays to ensure the manager meets basic operational obligations.

Managed fund fees and what they cover.

All of these fees — governance, custody, admin — are often deducted from the fund’s assets. Investors don’t see an invoice. Instead, these costs are netted off the unit price, subtly reducing the returns they receive.

These fees are disclosed, as required, in the fund’s Product Disclosure Statement (PDS) or Information Memorandum (IM). But the full picture only becomes clear in the fund’s annual financial report — where actual dollar amounts are recorded. These reports are available on request, but few investors seek them out. That’s a missed opportunity. The information is there — it just needs to be read.

Why does this matter? Because over time, even small annual costs compound. The Productivity Commission, in its 2019 review of the superannuation system, noted that a 0.5% difference in annual fees could reduce a typical worker’s final retirement balance by around 12% over a working life — a clear demonstration of how small, persistent costs quietly compound against investors.

Academic research tells the same story. In his 1991 paper The Arithmetic of Active Management, Nobel laureate William Sharpe demonstrated that the average investor underperforms the market by the amount of their costs. This is reflected in the SPIVA Australia Scorecards, which show that 80–90% of actively managed Australian equity funds underperform their benchmarks over 10- and 15-year periods — after fees.

To be clear, this isn’t about criticising fees or how others charge them. Fund structures vary for good reasons. But investors deserve clarity and alignment — to understand who is paying for what, and how those choices affect returns.

So what should investors do?

First, they — and their advisers — should go beyond the PDS or the IM. Seek out the fund’s financial report. Clarify whether fees like trustee, custody, and administration are absorbed by the manager or charged to the fund. A manager should be able to explain their cost structure clearly and confidently.

Second, fund managers can help by offering plain-English explanations of their pricing. Transparency doesn’t mean lower fees — it means investors know exactly what they’re paying and why. At Hamilton12, we made the decision to cover all governance, custody, and administration costs at the manager level because we believed it was fairer and more aligned with investor outcomes.

Finally, regulators might consider ways to encourage greater visibility of real-world fund costs. ASIC’s RG 97 has brought consistency, but there’s still room for clearer, simpler presentation of fee impact — particularly in dollar terms. The tools exist. We should help more investors use them.

In investing, markets go up and down — but fees are predictable. They can be measured, managed, and optimised. What matters most isn’t just what your fund earns. It’s what you keep.

Disclaimer

The information contained on this website is produced by Hamilton12 Pty Ltd (H12) ABN 72 626 045 412, AFS Representative #001298730, Corporate Authorised Representative of K2 Asset Management Ltd (ABN 95 085 445 094)., AFS License #: 244393.

Its contents are current to the date of the publication only and whilst all care has been taken in its preparation, H12 accepts no liability for errors or omissions. The application of its contents to specific situations (including case studies and projections) will depend upon each particular circumstance. The contents of this website have been prepared without taking into account the objectives or circumstances of any particular individual or entity and is intended for general information only.

Any opinions contained within this website are the author’s own and should not be considered the opinion of H12 or as advice.

Any H12 funds referenced on this website are issued by K2 Asset Management Ltd unless otherwise stated. An information memorandum for the funds referred to on this website can be requested at www.hamilton12.com or by contacting H12. You should consider the information memorandum before making a decision to acquire an interest in a fund.

H12 does not accept any responsibility and disclaims any liability whatsoever for loss caused to any party by reliance on the information on this website. Please note that past performance is not a reliable indicator of future performance. Any advice and information contained on this website is general only and has been prepared without taking into account any particular circumstances and needs of any party. Before acting on any advice or information on this website you should assess and seek advice on whether it is appropriate for your needs, financial situation and investment objectives. Investment decisions should not be made upon the basis of its past performance or distribution rate, or any rating given by a ratings agency, since each of these can vary. In addition, ratings need to be understood in the context of the full report issued by the ratings agency themselves.

The content of this website is not to be reproduced without permission.

All rights reserved Hamilton12 Pty Ltd (ABN 72 626 045 412).