All characters depicted are public figures in a fictional scene. Any resemblance to real policy tension is entirely intentional.

As Division 296 reshapes the superannuation landscape, investors must weigh the benefits of franking credits against the risks of portfolio concentration, and consider more efficient, diversified alternatives.

Since its introduction by the Hawke-Keating government in 1987, and further enhanced by the Howard government in 2000, Australia's dividend imputation system has helped investors avoid the double taxation of company profits: first at the corporate level, then again at the individual level. When a company pays tax on its earnings and distributes those profits via franked dividends, Australian investors receive a credit for the tax already paid. It is a feature of our tax system that continues to favour long-term investors, particularly superannuants and retirees.

With the proposed Division 296 legislation likely to take effect from 1 July 2025, the imputation system is once again in the spotlight, but for new reasons. Division 296 will impose an additional 15% tax on the earnings attributable to superannuation balances above $3 million. Importantly, the tax is calculated on a notional earnings figure that includes unrealised capital gains, rather than actual cashflows or distributions. It is a blunt measure that has understandably triggered a renewed search for tax offsets, especially among SMSF trustees.

One idea gaining traction is to increase exposure to high-franked Australian equities as a way to soften the blow. In practice, this means capturing franking credits within the fund and using them to neutralise the additional tax liability. Conceptually, it makes sense. But done poorly, it can introduce risk.

Let's take a closer look.

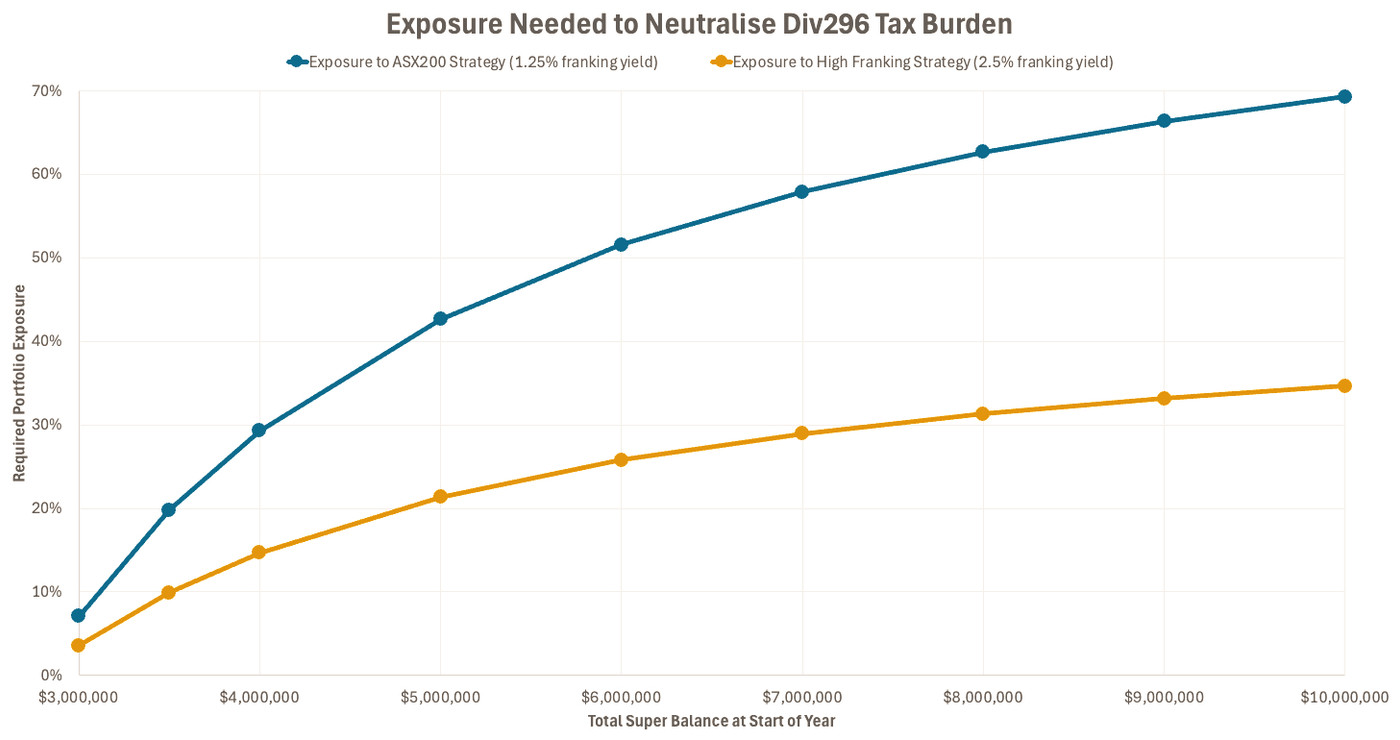

Consider an SMSF with a starting balance of $5 million earning 8% for the year. Under Division 296, approximately 44% of the fund's earnings are deemed to come from the portion of the balance above the $3 million threshold, triggering a tax liability of roughly $27,000. If the trustee attempted to offset that liability solely via an ASX200 ETF, with a current grossed-up yield of 5.2% and a franking credit yield of 1.25%, they would need to allocate 43% of the entire portfolio to that single strategy.

That level of concentration raises a red flag. While the ASX200 offers broad market exposure, only a subset of its constituents contribute meaningful franking credits. So the yield, and therefore the tax efficiency, is diluted.

Alternatively, if the same investor allocated capital to a more targeted high-yield, high-franking strategy with a 2.5% franking yield (and a gross yield of 8.5%), only 21% of the portfolio would be needed to fully offset the tax burden. That is half the exposure for the same tax benefit.

Now this is the part where I disclose my bias. At Hamilton12 we manage a tax-aware, high-franking equity income strategy for superannuation investors. So I do have a vested interest in how these ideas are received. But the maths is the maths, and I would be making the same point even if I did not spend my days thinking about it.

To keep the illustration simple, these examples exclude contributions and pension withdrawals. It is also worth noting that while franking credits used to offset Division 296 tax are beneficial, any excess franking credits will still increase the member's total superannuation balance (TSB). This in turn may lead to a higher future Division 296 liability. However, the value of the credit still outweighs the incremental tax, especially when comparing dollar-for-dollar outcomes.

There is, of course, an irony here: under Division 296, investors can end up being taxed on franking credits themselves because the credits contribute to the TSB, the very same balance on which the tax is calculated. It is a structural inconsistency that undermines the intent of the imputation system, which was designed to eliminate double taxation. But that is a discussion for another day.

As shown in the accompanying chart, the difference in required portfolio allocation becomes more pronounced as super balances grow. For a fund with $10 million, offsetting the Div296 tax using a standard ASX200 ETF would require nearly 70% of the portfolio. Using a more efficient, diversified high-franking strategy, the same outcome can be achieved with just 35%.

Illustrative only. Shows portfolio exposure needed to offset Division 296 tax at 8% change in TSB. High-franking strategies achieve this with far less concentration. Source: Hamilton12 analysis, June 2025.

In a world where after-tax returns matter more than ever, the temptation to load up on franked dividends is understandable. But as with any investment decision, execution is everything. Strategies that combine high yield with diversification offer a compelling way to optimise after-tax outcomes without compromising portfolio construction principles.

The tools are there. It is about using them wisely.